Since getting married earlier this month, we’ve been busy assembling a giant package of documentation for Rakhat’s US green card application. The insane complexity of an I-485 adjustment of status application is another article in and of itself (particularly given where we live), but we finally got the forms filled out, and all of the documentation and evidence assembled. So finally, with the application fully complete, I attached Form G-1450 on the top with my Capital One Venture X card details filled in. I felt pretty confident in doing this because I’d used the same card for our original I-129F application, and everything went through just fine. I even earned points for the transaction! We sent the application off on Monday.

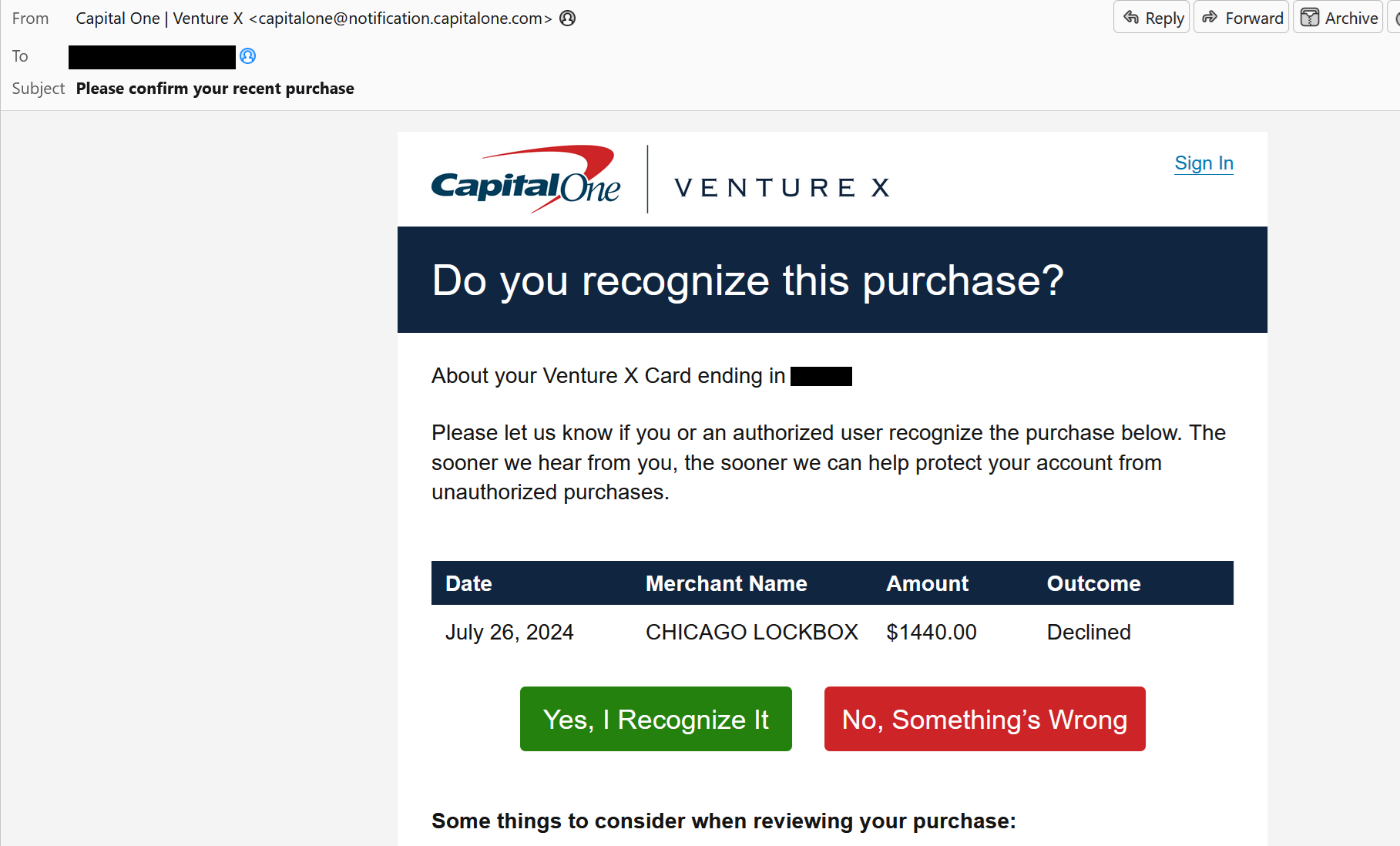

Yesterday afternoon, an email from Capital One rolled in: “Please confirm your recent purchase.” Uh-oh. I opened it up to see this:

I recognize the charge, and also, something is very wrong

Yes, I did recognize the purchase. It was the green card application fee. Why was it declined?

This is the most legitimate kind of charge possible. The kind that is basically never fraudulent. The charge was literally made by the federal government and there is essentially unlimited recourse against anyone making fraudulent payments to the government. Unless my account wasn’t in good standing, there would never be any legitimate reason to decline the charge. So, I thought maybe my autopay didn’t go through or something. Could it possibly be my fault?

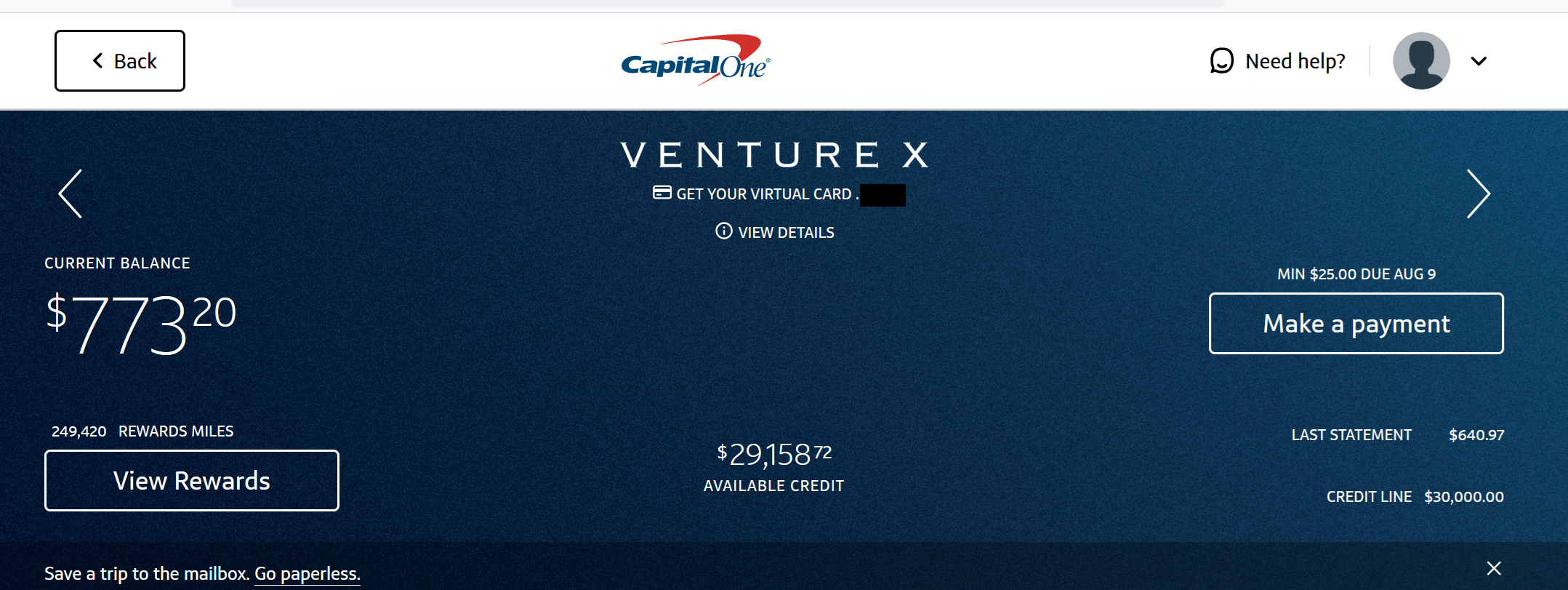

Nope, not my fault!

My account is current. I have over $29,000 in available credit. There’s nothing on my end that could possibly have caused this problem. However, Capital One laid off over 1,000 technology employees last year in a drive to replace them with AI. Don’t take it from me, you can read it on their own blog. So, as is increasingly common, Capital One has put dumb hallucinating AI bots in charge of important, serious things that have a very real impact on people’s lives. When this goes wrong, it goes spectacularly wrong.

The impact, of course, is significant. Immigration timelines are measured in months. We have to wait for our application to be returned, and file it all over again. Typically, this sort of unforced error will add 2 more months. In the meantime, Rakhat can’t leave the United States, and given where we live, this is a significant impact. There is only one flight a week to the US mainland. We don’t have a hospital, dentist or even a pharmacy here. It’s an extreme hardship that didn’t need to happen.

“Why did you trust Capital One?” some people will ask. “You should have sent a check!” Ironically, I made that decision to prevent fraud. Check fraud is rampant, and it’s a lot safer to use a credit card than to send a check in the mail these days. I won’t take the risk of a credit card transaction failing again, though, and will have to instead accept the risk of my checking account being drained by criminals.

In the meantime, should you trust Capital One for anything important or serious in your financial life–the kinds of things that absolutely, positively have to work? Given my experience, I cannot in good conscience recommend them. Their anti-fraud software product managers are bad at their job and should feel bad. Sure, use their card in retail situations where you can easily switch to another card if things go haywire. Their points program is exceptionally generous, and Capital One likely loses money on it. But don’t trust a Capital One card for anything that is truly important, and be sure to burn your points before they devalue.

One of the most touted benefits of Caesars Diamond status is that you can get a free stay at the Atlantis Bahamas. This is a destination I wouldn’t ever have normally considered, but there was a really good sale fare from Vancouver to Nassau so I grabbed tickets a couple of months ago. This is usually a rational strategy: if there is a good deal on flight tickets, just grab the flights immediately and figure out the rest later.

I had no idea what I was setting myself up for.

Looking at a picture is the closest you might come to staying at the Atlantis Bahamas

I called in December and was informed that the calendar wasn’t open yet for February. “Call back after the first of the year, and there should be good availability” said the friendly agent. OK, fine. I called in on January 2nd, and was informed that the calendar would be opening for February in mid-January, without any certainty as to exactly when. “I know this sounds crazy because it’s really soon, but call back after the 15th and we should be able to take care of you.”

OK, fine. I called back today, less than two weeks before my planned stay (starting on the 2nd of February). “Have you ever booked with us before?” Apparently there’s a process where the Atlantis has to confirm my benefit with Caesars, and that takes a couple of days, and they can’t make a reservation before then. But it doesn’t matter anyway, because the first 10 days of February are sold out. “Reservations have been open since Sunday,” the agent cooly stated. That’s funny, because the Web site says that reservations don’t open until February 1st.

Now, rooms aren’t actually sold out. You can buy all of the rooms you want. You just can’t use your Caesars benefit on those days. Atlantis manages its inventory like saver level frequent flier awards. They black out popular dates, and you’re more likely to be able to use the benefit for a midweek versus a weekend stay, and during hurricane season versus a nice time of the year to visit. While we all prefer different experiences when we travel, it’s personally difficult for me to justify using scarce vacation days on a destination like The Bahamas in order to stay in a casino resort.

So, I ended up spending 11,000 Choice points per night (transferred 1:2 from Citi) to stay in the Comfort Suites next door. They charge a $45 per night resort fee on top of it, so I spent the equivalent of $510 in points and cash for a 4 night stay. That stings, although it’s only 1/3 the cash rate for an equivalent room (Choice had availability for a garden view suite). There’s still a remote possibility that someone will cancel and I’ll be able to stay during my planned dates, but the possibility is remote.

Should you go for a Caesars Diamond status? Possibly, if it makes sense (I got my status matched from Wyndham, and I get my Wyndham status from a $95 annual fee credit card, which is less than I’d spend on parking each year at a conference I attend in Las Vegas). However, I wouldn’t gamble extra, or buy a Founder’s Card membership, with the intention of using this benefit. My experience actually trying to book and use the Atlantis Bahamas stay has shown that unless you’re willing to travel midweek in off peak months, this isn’t an easy benefit to use. Honestly, though, what should I have expected from a property named after a lost city? Maybe it doesn’t even exist.

Everywhere you look, you’ll see people promoting the Chase Ultimate Rewards program and points transfers to Hyatt. The love for Hyatt in the blogosphere seems unlimited, even though they have repeatedly devalued their loyalty program just like everyone else (both covertly, by raising the category of existing properties, and overtly, by shifting to a multi-tiered pricing model). Sure, Hyatt has some nice properties, but the majority of them are mediocre properties (many of which in the US are owned by the notoriously cheap operator Aimbridge Hospitality). Many of them don’t even clean your room. So the reality of Hyatt is that you’re paying higher prices for worse service, so it’s worth questioning the comparatively higher cash rates that they charge versus other properties. And this should factor into your calculations when spending points. Even if you’re spending points at a high return, if that return is up against a poor cash value, this isn’t a good use of points!

This brings up the hotel program that almost nobody talks about: Choice Privileges. I get it: the program is obscure. And yes, very few people would consider a Comfort Inn to be an aspirational property. Nevertheless, these are the exact kinds of properties that I spend actual cash on, and the cash prices are actually competitive. When I’m traveling, I am usually just looking for a clean comfortable room where I can get a good night’s sleep without breaking the bank.

Nobody would consider the Comfort Hotel Kanda to be aspirational, but does it really need to be? It’s just a 7 minute walk to Akihabara!

Here’s an example. The Comfort Hotel Tokyo Kanda costs 8,000 Choice Privileges points per night. That’s up against a JPY 17,700 rate on the weekends, which is $118.49. The property is just a 7 minute walk to Akihabara, which is one of my favorite neighborhoods in Tokyo. So if you were transferring points at 1:1, it’d be just shy of 1.5 cents per point which is a completely reasonable points redemption. It’s well above the Seat 31B weighted average realistic value of most points programs.

However, Citi ThankYou points transfer 1:2 to Choice Privileges, meaning that you’re paying just 4,000 Citi points per night. This yields a return just shy of 3 cents per point, and this isn’t some pie-in-the-sky valuation against cash you’d never actually spend. It’s close to 3 cents per point in value against a totally reasonable cash price that I’d be spending in Tokyo anyway, if not at this property, at another similar business hotel.

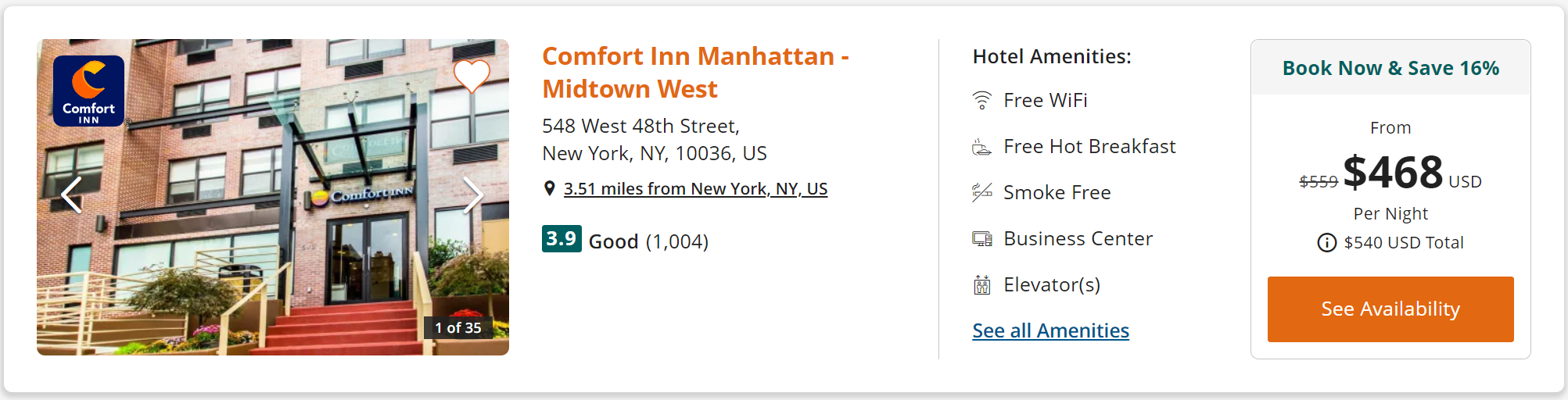

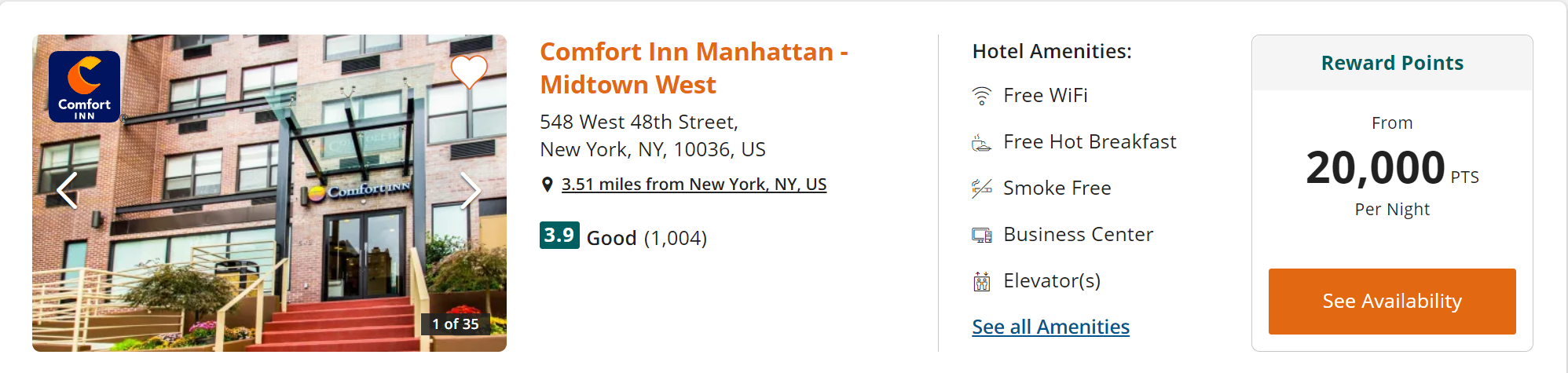

The value can be even greater than this. Take New Year’s Eve in New York. The Comfort Inn Manhattan-Midtown West is $540 per night all-in, cash rate:

If you’re paying with points, it’s 20,000 Choice Privileges points, or 10,000 Citi ThankYou points:

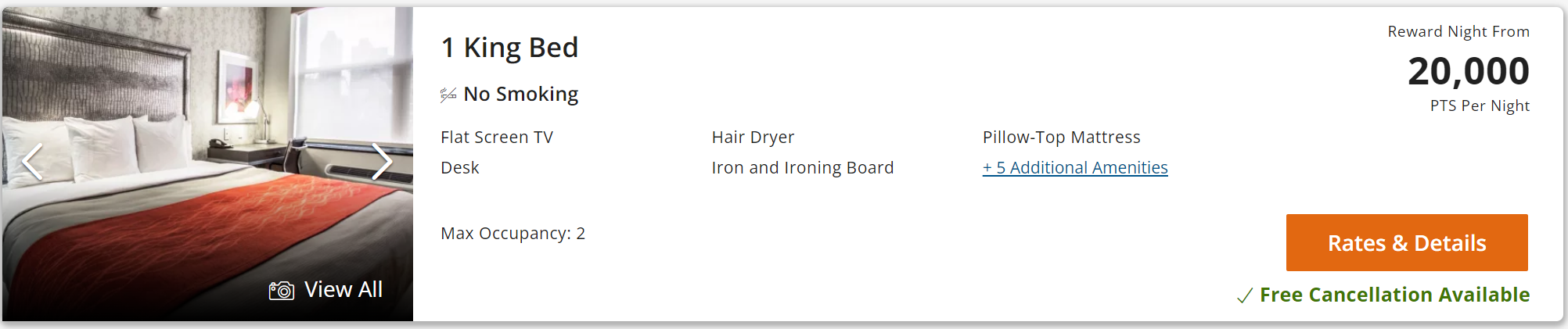

This isn’t just for the weird room every hotel on Manhattan seems to have. You know the one; it used to be a closet next to the elevator, and someone crammed a twin bed in there. You have your choice of two twin beds, a queen bed, or this swank king room:

This is a normal rate for New Year’s Eve in New York. It’s a completely reasonable property on Manhattan. And reserving through Choice Privileges delivers an absolutely astonishing 5.4 cents per point in value for your Citi ThankYou points. By the way, this inventory is live right now. You can go out and book it. If you go, send me pictures of the ball dropping in Times Square.

Now, I get it. Citi doesn’t pay fat commissions to bloggers like Chase does, so their cards are promoted less. Citi also has fewer cards in their ThankYou Rewards program, so it’s harder to churn through signup bonuses: you actually have to spend on their cards to earn ThankYou points. For the most part, there aren’t fancy splashy high annual fee cards in the program; in fact, Citi probably wins the “fewest perks” award for their card lineup (they don’t even offer secondary rental car insurance). So this program, in all likelihood, gets less attention than other programs.

Choice also doesn’t have fancy aspirational properties (their Ascend Collection brand, which are Choice’s highest end properties, are upper midrange at best). If you’re the kind of person who is excited more by the hotel where you’re staying than the destination you’re in, this program is probably not for you. You also can’t reserve more than 3 months in advance, so if you’re planning well in advance, it can be hard to use this program. Choice seems to manage their program to give away the rooms they don’t think they’ll sell, with an availability floor for rooms booked with points.

If you’re going to stay in a mediocre property anyway, wouldn’t you rather pay a price to match? Skip overpriced and dumpy Hyatt properties and consider a Choice or Wyndham hotel instead.

Nearly every airline program I work with at AwardCat has massively devalued. And yet, I keep seeing the same optimistic points valuations on every blog. In my view, valuations are mostly a lie. While it might be theoretically possible to achieve the valuations noted, it’s clear that for the majority of redemptions, points aren’t worth anywhere close to what is ordinarily claimed.

Working with a shadowy group of Pacific Northwest miles and points enthusiasts, I have created a points valuation chart using an entirely new methodology. The truth is, the value of points varies per redemption and a lot of the value is theoretical (tickets to Amsterdam are generally undesirable in February, even if they’re still expensive in paid business class relative to redeeming with points).

This chart focuses on flights, not hotels. There is one exception: I did factor in the value of Hyatt transfers from Chase, because these really can deliver outsize value. Other hotel programs usually aren’t good value in exchange for transferable points.

You can usually get better value when booking independent hotels versus transferring bank points to a hotel program

Along the same lines, some options for redeeming your points are really good value, and others are not. So, we tried to calculate a weighted average based on a mix of awards redeemed within the program (as most users do; it’s rare that anyone uses their points only for the most aspirational of journeys). We also defined ceilings: Realistic Ceiling and AspirationalCeiling, which reflect the highest value that can realistically be attained by most people, and the highest value that would typically be attained for an aspirational trip.

In particular, given the “ceiling” valuations, there are both objective and subjective influences and there’s probably room for folks to argue. For example, Aeromexico offers a tantalizing round-the-world award chart that should, in theory, offer far greater value than the 1.2 cent aspirational ceiling I have assigned. There are only two problems: partner availability is virtually nonexistent to Aeromexico on Korean Air, Delta, KLM and Air France in business class, and virtually all SkyTeam carriers levy fuel surcharges (along with Aeromexico itself). A round-the-world trip in economy class (with hefty fuel surcharges paid on every leg) looks a lot less aspirational, doesn’t it?

Conversely, Alaska Airlines crowns the aspirational ceiling (despite recent devaluations) because of their relatively low first class pricing, and because stopovers are permitted, achievable, and allowed on a one way trip. It’s harder than it used to be to take advantage of this, but stopovers really add outsize value. Air Canada similarly offers stopovers for 5,000 points each, although their comparatively high redemption rates lower their aspirational ceiling.

Airline/Program

Floor

Weighted Average

Realistic Ceiling

Aspirational Ceiling

Aeromexico

0.6

0.8

1.0

1.2

Air Canada

0.8

1.3

1.9

2.9

Alaska

0.8

1.3

2.1

4.2

American

1.2

1.4

2.2

4.0

Amex

0.7

1.1

1.4

2.9

Avios

0.7

1.1

1.8

2.2

Bilt

1.5

1.6

2.2

4.0

Brex

0.6

0.8

1.0

1.7

Capital One

1.0

1.3

1.7

2.9

Cathay Pacific

0.8

1.2

1.9

2.4

Chase

1.0

1.3

1.4

4.0

Citi

1.0

1.3

1.7

2.9

Delta

1.0

1.2

1.7

2

Emirates

0.6

0.9

1.1

1.4

Etihad

0.6

0.9

1.1

1.2

Flying Blue

0.8

1.1

1.6

1.8

jetBlue

1.2

1.2

1.3

1.3

LifeMiles

0.7

1.2

1.8

2.7

Qantas

0.5

1.0

1.2

3.9

Singapore

0.8

1.0

1.3

1.7

Southwest Airlines

1.2

1.3

1.4

1.4

Turkish

1.1

1.5

2.4

2.4

United

1.0

1.2

1.8

2.2

Virgin

0.8

1.0

1.4

2.2

Average across all programs

0.9

1.2

1.6

2.48

The above chart reflects my personal opinion of what airline and transferable points are worth, and is not the expressed opinion of AwardCat or any other party.

One of the biggest surprises to all of us was the low “floor value” of most points. This is because airlines and banks offer a lot of really unoptimal ways to spend points, from paying for WiFi charges to buying gift cards or statement credits towards credit card purchases. I ignored some of the worst and least optimal ways to redeem points and focused on flight related redemptions (either flights or enhancements to the onboard experience). Southwest and jetBlue win here, because it’s hard to spend your points for less than 1.2 cents each. While Turkish comes in just behind, this is primarily because there just aren’t very many ways (yet) to spend your points unoptimally in this program. And Brex (which, full disclosure, fired AwardCat as a customer so I do hold a grudge) takes the crown for least valuable transferable points. I’m very happy to have transferred my points out before they suddenly devalued their points with zero prior notice. That’s the risk you take with bank points, as I warned in 2016.

While again highly subjective, I think the weighted average is where most people are likely to redeem their points. This is surprisingly low. Some programs, such as Emirates and Etihad, have so hugely devalued their programs that their points average less than one cent apiece in redemption value. Singapore maintains a relatively low weighted average because of their high redemption rates for economy class flights, and their levying of fuel surcharges on partner flights. And the weighted average of bank points is about 30% more than their floor value because of the optionality for points transfers that they provide. I will point out that Chase’s own valuation of Ultimate Rewards points, when redeemed through their portal for travel, would seemingly (net of the likely profit gained by running their own travel agency) agree with ours.

Wrap-Up

I think that most sources online offer an overly rosy picture of the value miles and points can have. Now, I won’t say it’s because most of them financially benefit from you remaining invested in these programs, or that credit card links can pay hundreds of dollars in commissions. So, maybe they just haven’t updated their assigned valuations to account for the massive inflation in award costs? Or maybe they believe that when airlines and hotel chains assign a possible range of award costs, lower pricing will prevail more often than higher pricing (also, if you believe that, I have a bridge to sell you)? Maybe they just really value the optionality of transferable points, to the extent that this optionality is worth considerably more than the points of transfer partners? Whatever reasons they have for their charts, here is mine. This is what I think points are really worth, for most people, most of the time, under most circumstances.

Do you agree? Vehemently disagree? Leave your comments below!

I don’t prefer to stay in chain hotels, and they often don’t exist anyway in the off-the-beaten-path places where I prefer to travel. However, I go to a conference every year in Las Vegas where I run an event. Now, Las Vegas is probably my least favorite destination in the world, and I’d probably never visit otherwise if not for this particular conference. Naturally it happens in the summer, also happens to be during a peak travel week (for some reason), and this makes both flights and hotels really expensive.

Once you have seen the lights of Las Vegas once, you don’t ever need to go back

This year, I somehow managed to get a cheap flight (Southwest ran a good sale after their massive meltdown, so I burned some of my Rapid Rewards points) and the next challenge was finding a reasonably priced hotel. Las Vegas has gotten incredibly expensive as of late. Everything costs extra. You’ll typically pay $30 per day (or more) in resort fees, and on top of this, there’s $15 or so in parking charges. And that’s on top of the rate, which is often $150 or more. A cup of coffee costs $7 (not a fancy barista beverage, just plain coffee). The days of cheap deals in Las Vegas are over.

While I typically use miles and points for flights, there are occasional good values with hotels. The most well-known program is Hyatt, but there was just a brutal devaluation earlier this month, which is a follow-on to the gut punch of a devaluation last year. In Las Vegas, this means you can now book a room at a Hyatt Place for 15,000 points (worth an eye-popping $187.50 worth of Chase points) per night. Plus parking. I’m sorry, Hyatt, but I haven’t stayed at a Hyatt Place anywhere in the world that is even close to worth that.

I checked with a friend who works at a Strip hotel. He offered me his friends and family rate of $249 per night, plus resort fee. Thanks but no thanks. Grasping at straws, I looked at IHG who wanted close to $300 per night worth of points (at current sale prices) for a room at a Holiday Inn Express. And then, bearing in mind my terrible experience at the La Quinta last year (I consider it one of the worst hotels in Las Vegas–check the reviews), I decided to see what Wyndham had to offer.

Transferring Points To Wyndham

Most people don’t know this, but you can transfer both Citi ThankYou and Capital One points to Wyndham. The program offers two different redemption options: “Go Fast” which offers a discounted room rate plus a small number of points (either 1,500, 3,000 or 6,000), and “Go Free” which offers a completely free room paid entirely with points. Most properties cost 15,000 points per night, including such renowned brands as Travelodge and Days Inn. Some top tier (for Wyndham) properties cost 30,000 points. You can also book Vacasa vacation rental properties at 15,000 points per bedroom per night, which can be a pretty good deal in expensive resort destinations. Now, you’re reading Seat 31B, and you can probably guess that $187.50 worth of points (and up) isn’t what I typically spend on a hotel night. There are, however, a handful of properties that cost only 7,500 points per night, and this is where you might occasionally strike gold in the Wyndham program.

In Las Vegas, Wyndham owns a resort called the Desert Rose. It has a two night minimum stay, and is really well rated. Even though the property is actually a resort, they don’t charge for parking or have a resort fee. What’s more, for some reason, this property costs only 7,500 points per night for a “Go Free” stay. But it gets even more interesting than that. Their “Go Fast” rate is actually variable during the week, while paid stays don’t vary much (you’ll pay about $150 per night during the week, and $185 per night on the weekends). “Go Fast” stays from Sunday through Thursday were averaging out at 1,500 points plus less than $70 a night!

Splitting Up Stays

One tactic I’ll sometimes use is paying for some nights, and using points for another. In this case, on a one week stay, the best deal was to use the “Go Fast” rate for Monday through Thursday nights (spending an additional 6,000 points for a completely free room would yield less than $70 in savings, or about 1.1 cents per point). I then booked the “Go Free” rate for Friday through Sunday nights (where I’d have had to spend much more out of pocket, yielding over 2 cents per point in value overall). This meant making two different reservations and technically I will have to check in and out mid-stay. However, hotel front desks are used to dealing with this sort of thing (which can happen for various reasons) and can usually put two reservations together so you don’t have to change rooms.

Wyndham Is Weird

Look, Wyndham Rewards is a pretty strange program, which I suppose suits a hotel chain as strange as Wyndham. They have a pretty big footprint, but their properties are mostly a random hodgepodge of truck stop motels and the occasional timeshare resort. Quality is all over the place, with very little consistency even within brands, and few people would ever consider a Days Inn to be aspirational, which is why I think there is very little written about Wyndham Rewards. Pricing is also all over the place in the program. It’s usually not very good, but occasionally, it’s incredibly good.

I still prefer not to stay in chain hotels, but I like spending money even less (at least when I could spend points at good value). It’s hard to find good independent properties in a place like Las Vegas anyway, and I was happy to get some incredible value for this stay. With no resort fees, no parking fees, and an all-in effective room rate of under $100 per night at a non-casino resort property in a good location, I think this deal has earned the Seat 31B seal of approval.

Chase pays some of the highest commissions in the blogosphere. It can be hundreds of dollars per card signup. The travel blogging community is overall pretty friendly, but nothing is played closer to the vest than highly coveted Chase affiliate links. Nothing can financially make or break a travel blogger faster than Chase either granting or revoking sponsorship. And that’s why you will hardly ever see anything negative written about Chase. All you ever hear is whispers, but word on the street is Chase doesn’t like criticism. They don’t ever want to see anything negative. So, if you know what’s good for you, and you don’t want to be blackballed by Chase, then you’d better stick to the talking points.

And that’s why Chase has probably been able to skate for so long on their absolute disaster of a travel portal. It’s a hot mess and after having spent over 3 hours of my Seychelles vacation banging my head against the wall in trying (and failing) to book a 40 minute roundtrip flight, I am mad as hell and I’m not gonna take it anymore! And I am writing it with the full realization that it might not even get read, while potentially costing me thousands of dollars in commissions.

Higher Prices

The Chase travel portal is operated by Expedia. You would think that this means that they offer the same prices as on expedia.com, but they don’t. The prices are usually higher on the Chase portal.

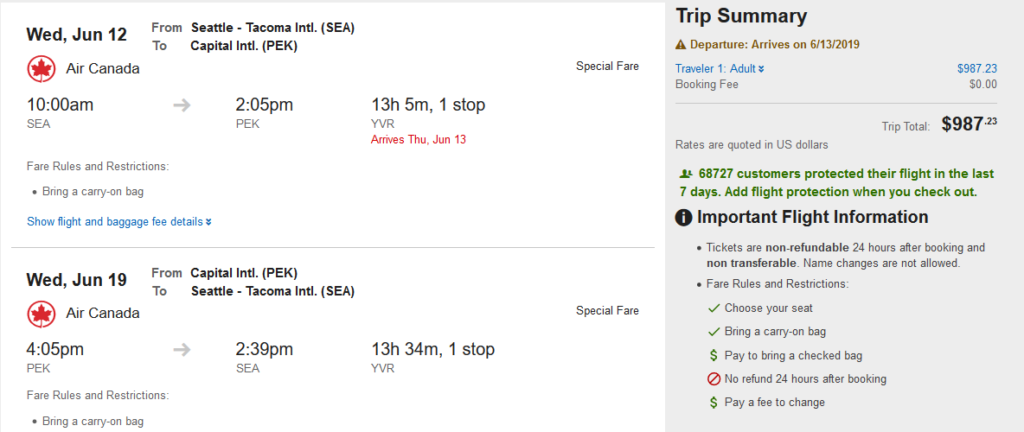

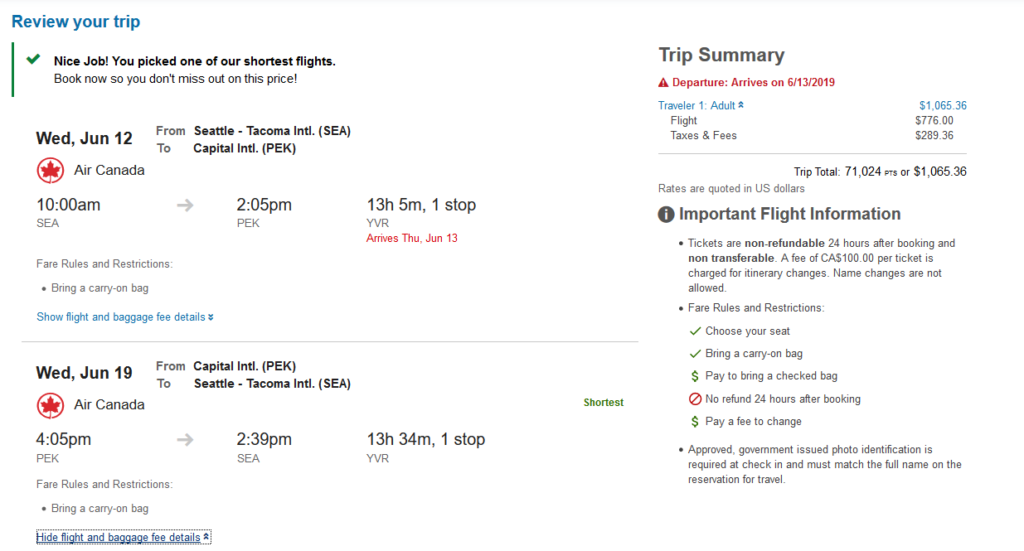

I’m answering a lot of questions from friends lately about flights to Beijing for DEF CON China, so I picked this route at random (but for different dates). This problem is so widespread that literally the first flight I looked at cost more. This example is for Seattle to Beijing, departing June 12th, returning June 19th.

Let’s start with the price on Expedia:

$987 on Expedia. Note this is higher than the $946 price booking direct with Air Canada.

Now let’s check the Chase portal:

Same flights, $78 higher price.

The Chase portal price for the above example is $78 more. The flight I was looking at booking today (but failed to book) between Mahe Island and Praslin Island in the Seychelles was $168.60 booked through the Chase portal, but $151.07 booked directly though the airline. While domestic US flights are generally priced about the same as the Expedia price, international flights, in my experience, tend to run about 10% more. This sucks a significant part of the value out of the points you have earned.

It’s not just flights that are more expensive when booked through the Chase portal. Rental cars can be significantly more expensive. Hotels are also often more expensive.

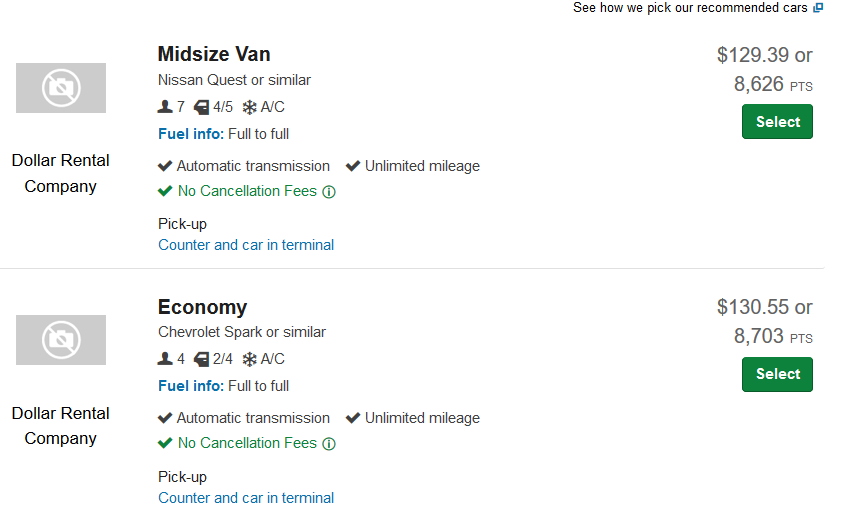

To underscore this, I’ll use a trip I’m taking in a few weeks as another example. Here’s the current best rate available through the Chase portal for a car from Dollar Rent A Car:

I don’t get why a minivan is cheaper, but we’ll roll with it

Here’s the deal for a “specialty vehicle” (which will probably be a minivan) that I locked in on Priceline. At the time I booked this, cross-checking with Chase yielded an even higher price than is currently offered:

Chase jacks up the rate by almost 30%. If you have the Chase Sapphire Preferred, spending your points this way versus just going for a statement credit at 1 cent per point actually costs you money.

Not All Flights Are Bookable, Even When They Appear On The Portal:

OK, so you’ve decided that you’ll let Chase overcharge you for a flight so you can at least spend the points, while getting 10% less value than you expected. NOPE! The site is rife with technical glitches. Here’s what happened when I tried to buy a flight from Mahe Island to Praslin Island in The Seychelles. The flight appears on the Chase portal. It shows up on Expedia, too. Air Seychelles isn’t some sort of budget carrier or third-tier airline; it’s part-owned by Etihad and uses Etihad Guest as its frequent flier program. It’s the primary airline in a popular (and high-end) holiday desination. While it was $17.53 more to book with the Chase portal, I decided that I’d overlook it.

Ha! Just kidding! I’d select my flights, put in all of my information, get all the way through to the end, and then the following error message would appear:

What payment information? I was paying entirely with points!

That leads to the next problem, which is…

Chase Travel Customer Service Is Terrible

The agents at Chase Travel (which is really Expedia) basically just use the Web site for you. If you have an error on the site, they’ll have the exact same error. They’re unable to deal with any situations that don’t fit the script. And they are on a very strict call timer with every incentive to get you out of their queue as quickly as possible. You are a hot potato, and all they want to do is get you out of their hands.

My first call had no resolution, so I became a hot potato. Chase Travel bounced me over to the bank. Call handling metrics good! The Chase agent was patient and helpful (they’re pretty good on the banking side), looked up my account, and verified that there were no issues that would prevent me from using my account. She transferred me back to Chase Travel. Call handling time minimized! The agent, after spending 3 minutes trying to convince me to “just wait a few hours and try again” had the same problem, and transferred me to something called the “legacy team.” Out of their queue! The “legacy team” agent took my information, we got all the way to the end, and….

…the call dropped. At this point I was into this for close to 2 hours, and I didn’t want to spend any more time on the problem, especially since the Internet connection (which slows down later in the morning–limited bandwidth on the island) was getting really choppy.

I tried again the next day. Another agent had the same problem, and tried to transfer me to the “legacy department.” After a few minutes, she came back on the line and asked me for permission to blind transfer me. I called her on it, but she blind transferred me anyway–into a queue of agents in The Philippines, which wasn’t the correct department. This was now my third agent in the same department (“New Platform”) who ran into the exact same problem. Mind you, I’m giving my name, flight numbers, and listening to disclaimers about non-refundable tickets each of these times. Finally, the Filipino agent got someone in the “legacy department” to have a try, and that agent couldn’t fix the problem either. So, in the end, hours into the problem, the agent offered a creative solution: I could book directly with the airline, and get reimbursed at 1 cent per point.

Yes, because Chase is incapable of selling me a flight, I should apparently lose the 50% bonus–which, I’ll note, I pay a $450 annual fee to receive. Ultimately, the agent gave me a 5,000 point “courtesy credit” but this is now on my record. Chase has a history of “firing” customers it thinks are costing them too much and I have now poked the dragon.

Wrap-Up

It’s not a secret that the new Chase travel portal is terrible. It’s terrible, horrible, no good andvery bad. But you’re only going to read about the problems with it here.

I ultimately don’t think that Chase being so thin-skinned helps them. They’re positioning the Chase Sapphire Reserve up against the American Express Platinum card, a truly premium card from a company with a lot of experience offering one and the global infrastructure (including a worldwide network of local offices) to match. Chase has third-party agents in Manila working “on behalf of” Expedia, a partner who may have been selected because they pay the highest rebates. And those third-party agents have only one mandate: get you off the phone, as quickly as possible. This isn’t the service I expect from a credit card with a $450 annual fee. If I want to spend the points I go out of my way to earn by putting a Chase card at the top of my wallet, I want it to “just work” as advertised. And I also don’t want to play shell games with disappearing partners, devaluing points and deceptive pricing. Chase, if you’re reading this–listen, I have a lot of respect for you guys. You’re brilliant at marketing. But the product ultimately has to measure up, and right now, it isn’t measuring up. Given the increased churn I expect this issue to cause, you’re about to get kicked in the NPV of your LTV.

I needed to take a last-minute business trip to Kiev. Cash fares were hovering over $900 one way for one-stop itineraries, so I started looking for opportunities to use points. When I book my own award travel, I optimize for the most efficient use of points and the stand-out value was 25,000 Ultimate Rewards points for an Air France flight. There was a long layover in Paris, but I really like Paris so the 9 hour layover was fine. It’s enough time to visit the Louvre and enjoy a coffee in a sidewalk cafe.

Unlike most airlines, Air France touts their economy class cabin. We’ll see if it lives up to the hype!

Unfortunately, the Flying Blue program is an absolute disasterright now. Air France/KLM just switched the chart from a fixed value redemption chart to variable redemptions (which, based on my analysis, is one of the biggest airline devaluations in history–most awards are up a minimum 30% and some are up 500%). It was a total fluke that the flight I wanted still cost 25,000 points, yielding 3.2 cents per point in value all-in (net of taxes/fees I had to pay out of pocket). This is very good redemption value on a ticket for which I would have paid real money. However, the devaluation comes on top of another negative change, removing the award calendar, which has driven call center volumes through the roof (because the only way to search for availability over a range of dates is to call now). Because of this, it can now take 2 hours to get through to an Air France representative.

Of course, my worst nightmare happened. Rather than posting immediately, after I transferred my Chase points, the points didn’t show up. I called Chase, who said that they transferred the points and it was Flying Blue’s fault. I called Flying Blue, and they said they hadn’t received the points so it was Chase’s fault. Both suggested I just wait. So I waited, and waited, and waited. I called to put the seats on hold so they wouldn’t disappear while I was waiting. Eventually I gave up and went to bed.

The following morning, the points still weren’t there. 4 hours before the flight, they still weren’t, so I called Flying Blue again. Fortunately, the friendly representative in the Mexico-based call center had a solution: “We are aware of this issue so we will advance you the points and your account will have a negative balance. When the points post from Chase, your balance will go back to zero.” She put me on hold, then came back a few minutes later to collect my credit card number. And just like that, I had a ticket to Kiev! I didn’t really believe that I did until I went to check in, and the computer spat out boarding passes.

So, certainly a stressful beginning to a trip, but a happy ending. I have no status with Flying Blue. I have never booked a ticket in their program. They don’t know I write this blog. They just thought on their feet and solved the problem by taking a risk (I could have been lying about transferring the points). And so instead of stranding me, which is totally what I expected, I’m now on the way to Kiev.

Summary

Chase is now reading a new telephone script when you call: “It can take from 1-7 days for your points to post after they are transferred.” After slowing down transfers to Korean Air and now Flying Blue, it appears Chase is trying to make Ultimate Rewards less valuable by making it impossible to redeem them for last-minute flights. This doesn’t appear to be a technical glitch; based on the policy change being communicated by their telephone agents, it seems to be deliberate. Also, there is nothing in writing on Chase’s Web sites to communicate the change, so people are going into this process with no idea that points transfers are no longer instantaneous.

Generally speaking, I like the Chase Ultimate Rewards program better than American Express Membership Rewards. However, the ability to have immediate use of transferred points is key. Award travel inventory is dynamic (a seat that is available now likely won’t be in a couple of days, particularly to a popular destination) and most of the value in keeping your points with a bank program instead of an airline program comes from the immediate ability to transfer and redeem points. There are fewer reasons to collect bank points instead of airline points if you aren’t able to easily redeem them for awards.

Airline points programs are rapidly losing credibility so it would be bad for consumers if banks to go the same direction and make points harder to redeem.

I have been catching up on my mail since returning from St. Helena and South Africa, and finally got around to opening the stuff that looks like junk mail. Of course, a lot of that stuff in there is actually important, and in the miles and points world, this is pretty explosive. It’s the first notice of an overt (rather than stealth) devaluation of a bank rewards program I have ever seen.

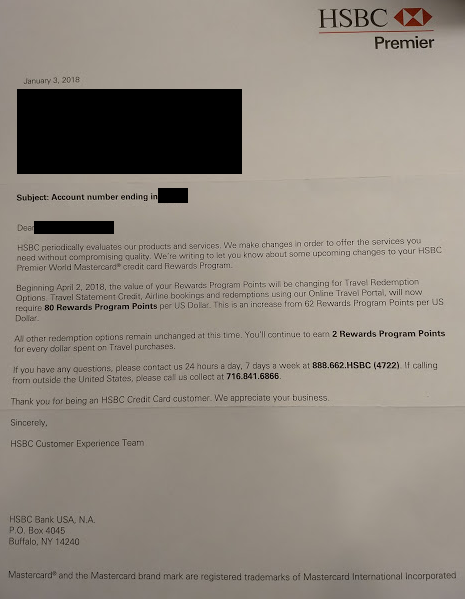

HSBC points are devaluing. Is the money in your account next?

Points in the HSBC Premier World MasterCard Rewards program spend like cash through a travel portal, similar to the US Bank or Bank of America rewards programs. Currently, for HSBC Premier members, the rate is 62 points per $1. However, as of April 2, 2018, the rate will increase to 80 points per $1. This is a significant devaluation, from about 1.6 cents per point in value down to 1.25 cents per point in value.

I think this is most significant because it is the first major bank program devaluation. Banks have been fairly hesitant to devalue their award programs, and I think for good reason. You don’t want to associate a bank’s brand with the idea that your assets in that bank will lose value. In fact, American Express has responded to airline award program devaluations by offering periodic transfer bonuses into airline programs. This has helped to maintain the value of Membership Rewards points.

However, HSBC crunched the numbers and must have decided that a money grab is worth the reputational risk. It’s an extremely aggressive move, because this impacts their Premier product–these accounts are for their highest value customers with over $100,000 on deposit. So, I think this is a shot over the bow. If HSBC is willing to devalue their points this much, and to do so for their highest value customers, I don’t think any bank award program is safe.

For my part, I’ll be asking my HSBC banker whether they also plan to devalue the cash in my account.