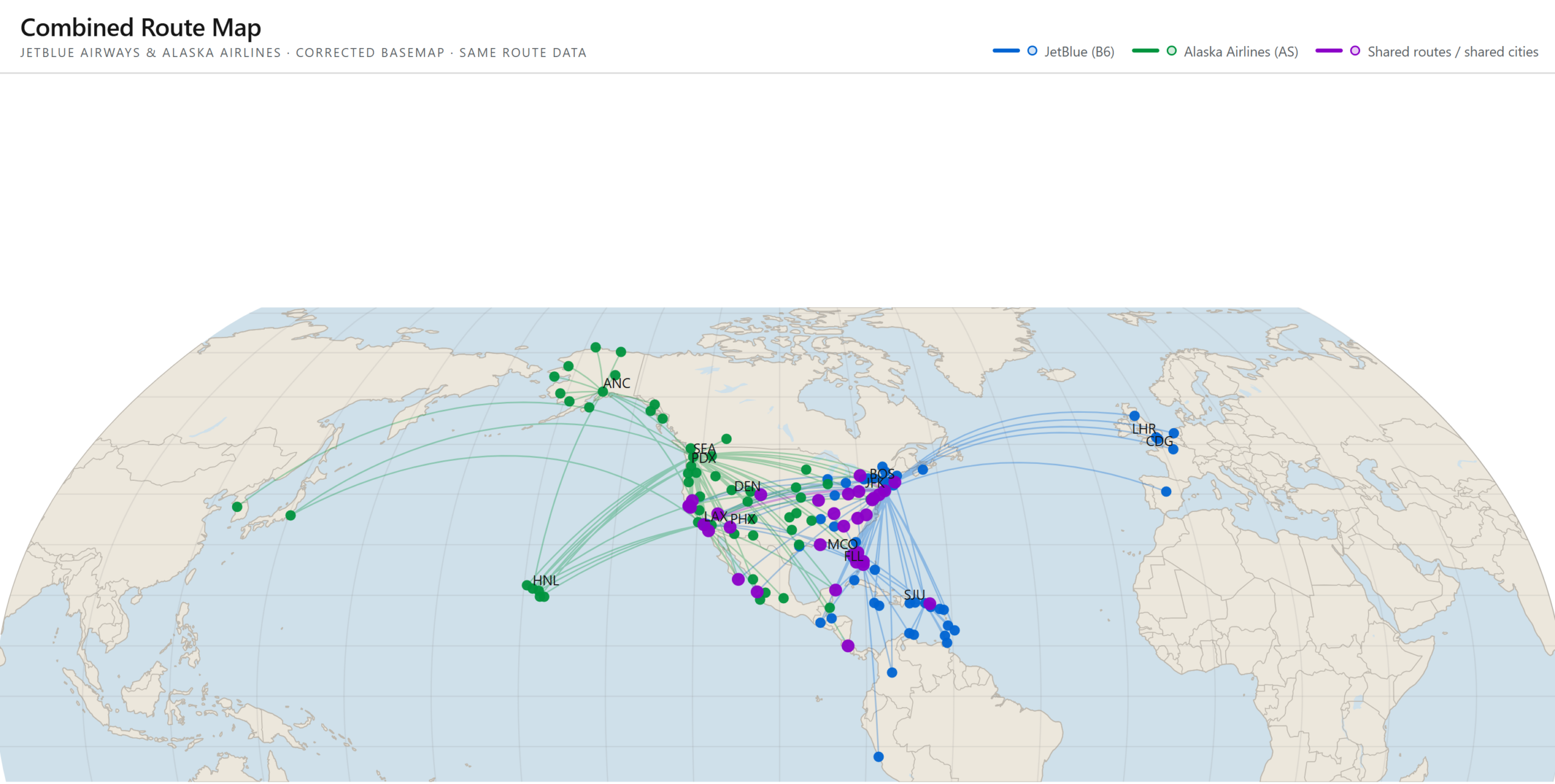

A lot of people seem very excited about the idea of Alaska buying JetBlue. I get it. The combined route map looks pretty compelling. Buying jetBlue would give Alaska a strong position in Boston, JFK, Fort Lauderdale, and San Juan along with a much bigger East Coast presence. JetBlue would have a buyer that is actually competent and not currently on fire. Executives would get to draw arrows on a PowerPoint slide and talk about a stronger fifth airline. What’s not to love?

There is only one problem. JetBlue is still JetBlue. This matters, because airlines are not just route maps. They are fleets, leases, labor agreements, debt, airport slots, loyalty programs, and IT enterprises (to name a few) with all of the associated financial machinery. And once you look at JetBlue that way, the case for a merger looks a lot less compelling.

There are real assets at jetBlue. Mint is a strong premium product, which is something Alaska is still learning to deliver. Boston is useful. JFK slots are useful. The A321LR is a very nice airplane for the kind of thinner transatlantic routes JetBlue has been flying, and Alaska does not really have an East Coast answer to that today. Alaska, meanwhile, now has Hawaiian’s long-haul platform and is trying to turn Seattle into a genuine international gateway. So yes, there is definitely an airline nerd case for this. The combined airline would make more sense on paper than a lot of other merger rumors do (such as Southwest buying Spirit).

But there is also a balance-sheet case against it, and that one is much less fun. In 2025, jetBlue lost $602 million and expects roughly $580 million of interest expense alone this year (I had to double check this number, because it’s so bad I almost didn’t believe it was real). Think about it: nearly six hundred million dollars just to service debt. The red ink is nearly as bad as the federal government, but jetBlue can’t fix it by raising taxes.

JetBlue has also borrowed heavily against TrueBlue, which means the loyalty program is not just sitting there waiting to be neatly combined with Alaska’s new Atmos setup. It already has a large (and incredibly toxic) financing structure hanging off of it, which is exactly the sort of thing that makes “obvious synergies” less obvious very quickly. This matters because the bullish version of this deal always sounds the same. Alaska gets Boston. Alaska gets JFK. Alaska gets Mint. Alaska becomes a real bi-coastal airline. Fine. I understand the pitch. But even the supposedly obvious prizes come with some pretty big asterisks.

Take JFK. People keep talking about JetBlue’s New York position as if Alaska would just buy the airline and inherit a clean pile of slots and relevance. But JetBlue already has the Blue Sky partnership with United, and that deal includes JetBlue giving United access to up to seven daily JFK roundtrips starting in 2027. So even the “buy JetBlue, get JFK” story is not nearly as easy as it sounds once you stop looking at a route map and start reading the paperwork.

The fleet story is the same way. Ten years ago, Alaska buying a big Airbus operator would have sounded absurd. In 2026 it sounds less absurd, but still annoying. Alaska already crossed the old Boeing-only purity line when it bought Virgin America. It crossed it again recently when it merged with Hawaiian, and Hawaiian brought Airbus A330s and A321neos with it. So the Airbus question is no longer existential. It is just expensive and messy. JetBlue’s current fleet is all-Airbus, and adds three entirely new types: A220s, A321neos and A321LRs in the mix. Some of those airplanes are absolutely worth having, especially the a220s (which would be perfect for inter-island flying in Hawaii along with seasonal intra-Alaska flying) and long-range A321s. But Alaska also just placed its largest-ever order for 105 737-10s and five 787s. Virgin America was a much less complex acquisition, and it still took years to sort out the fleet.

And then there is a morass of regulatory approvals, which is where merger proposals usually go to die. Alaska had a pretty smooth ride with Hawaiian. JetBlue has been having the opposite experience with its proposals. The Northeast Alliance with American was struck down, and the First Circuit upheld that ruling. Their planned Spirit deal got blocked too. So yes, I think Alaska-JetBlue is easier to defend than JetBlue-Spirit was. It is more end-to-end, less obviously destructive, and Alaska is not Spirit. But “better antitrust story” is not the same thing as “easy approval.” Not in this industry, and definitely not with JetBlue’s recent history.

If you are Alaska, the strategic case is obvious enough. Boston and a stronger East Coast presence is complementary. Scaling the Mint product would make Alaska internationally competitive. The airline-nerd deck practically writes itself. The shareholder case, however, is where the mood changes. Alaska just finished integrating Hawaiian onto a single operating certificate. It generated $1.2 billion in operating cash flow last year and is already in the middle of a huge fleet and network build-out. That is a bad time to take on JetBlue’s debt stack, JetBlue’s interest bill, JetBlue’s toxic swamp of loyalty-program financing, and JetBlue’s next several years of messy cleanup.

This is why I keep landing in the same place. Alaska should absolutely be interested in the pieces, if they can be separated from the business of jetBlue which is more or less toxic waste. The problems at jetBlue start with an impossible debt swamp, and it’s turtles all the way down. Alaska buying JetBlue’s problems sounds like the sort of thing that gets called “transformational” right before shareholders discover what their value has transformed into.

That leaves Alaska with a fairly obvious play.

Do nothing right now. Let Chapter 11 do what Chapter 11 is for. Let the balance sheet get cleaned up. Let the bad leases get dealt with. Let the lenders, lessors, and everyone else with a claim on JetBlue spend some quality time being somebody else’s problem. Let the financing structure around TrueBlue get untangled before Alaska goes anywhere near it. Then (and only then) Alaska can look at what is left and decide whether or not the price makes sense.

And if that happens, the case gets much better very quickly. A jetBlue acquisition starts to look a lot less like an act of charity and more like a smart expansion. Alaska already has the West Coast. It already has Hawaiian’s long-haul platform. It is already building Seattle into something bigger than a strong local hub. Add a cleaned-up JetBlue to that equation and suddenly Alaska is no longer trying to be a national airline from the west coast. It will have both coasts covered.

So yes, I can see Alaska and JetBlue fitting together one day. I just do not think the sensible version starts with Alaska volunteering to inherit all of JetBlue’s problems. Let bankruptcy court do the ugly work first. Then buy the airline that is left, not the one that needs saving.