Canadian startup low cost carriers have a checkered history in Canada. The first low cost Canadian carrier I flew was Canada 3000, which went out of business in 2001.

Canada 3000’s seating configuration was so dense that they might have been trying to fit 3,000 people on the plane

Many other attempts at low cost carriers have failed: Zip, Zoom, and Jetsgo. Even Air Canada couldn’t make the concept work, and retired their Tango subsidiary (although their cheapest economy class fares are still called “Tango”). The low cost carrier concept stubbornly keeps failing over and over in Canada, which is hardly surprising given that airport operating costs are some of the highest in the world (a report to the Canadian Senate in 2012 detailed myriad structural issues, and essentially nothing has been done or fixed since–in fact, operating costs have only gotten higher).

Nevertheless, startup airlines in Canada continue to open, fly for awhile, and then abruptly fail (usually leaving passengers stranded). The shakiest of these is currently Flair, which apparently didn’t have the money to take delivery of 11 new Boeing jets it had ordered, and which recently had four of its jets seized for non-payment of leasing fees. The 20% on-time performance rating for their Abbotsford-Calgary route is fairly representative.

So, did I book with Flair? Of course not! They weren’t the cheapest, and this article is about the cheapest airline in Canada. As it turns out, that’s tiny airline startup Lynx Air, which is currently flying a fleet of six aircraft. I had never heard of Lynx, but they popped up when I ran a search on an online booking site. I instead booked directly with the airline on their sketchy-looking Web site, and got back an email confirmation that looked like a phishing scam:

However, clicking on the attachment revealed an itinerary that looked like it was from circa 2003, using a random assortment of fonts that looked like a ransom note, and confirming that I had a roundtrip ticket to Calgary over March break weekend for CAD $168.00.

This is virtually unheard of; other airlines were charging well over $300 each way. I’m not sure whether Lynx forgot that it was a school holiday or what, but I really wasn’t going to question it.

The fare breakdown was as follows:

That’s right, roughly half of the roundtrip airfare went to airport fees, and that’s before the airline’s share of the operating costs. Lynx would definitely be losing money on me.

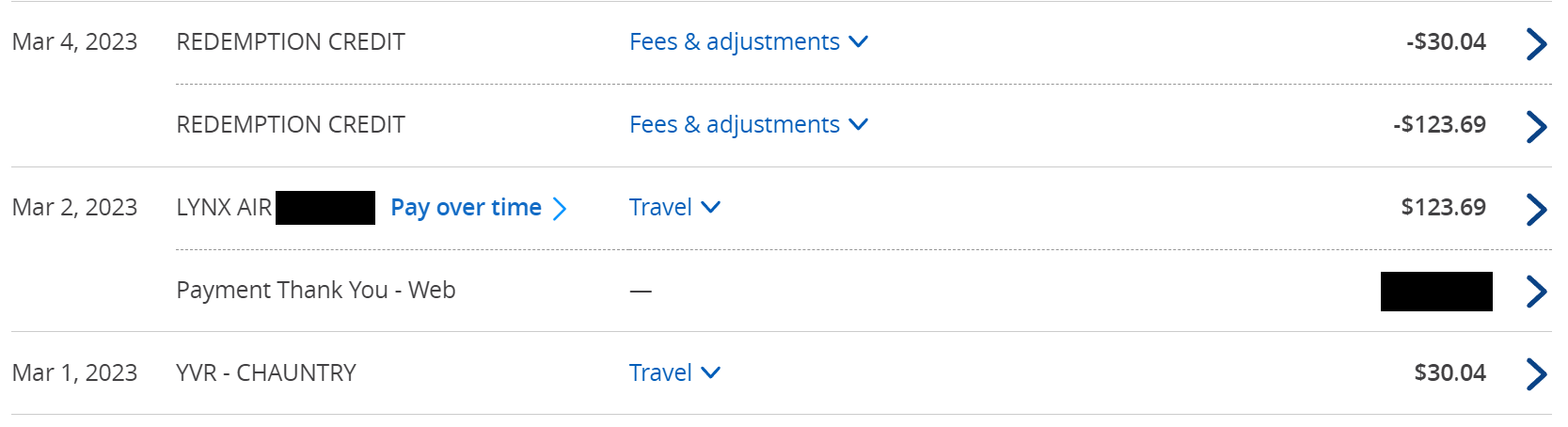

“But wait,” you might say, “the headline says you paid with Aeroplan points. How did that work?” Well, I have the Chase Aeroplan credit card. A few months ago, Chase was offering a 30% bonus to transfer points into Aeroplan, and if you have the credit card and transfer 50,000 Chase Ultimate Rewards points or more into Aeroplan, you got another 10% bonus on top of it. So I ended up with 70,000 points in Aeroplan. Well, in February, Chase decided to be exceptionally generous and started a promotion. You can now redeem Aeroplan points towards travel purchases (literally anything that codes as travel) at 1.25 cents per point. This meant that I could effectively spend the Ultimate Rewards points I transferred for 1.75 cents per point in value.

And that’s exactly what I did, as soon as the charge posted to my Chase Aeroplan credit card account:

I went ahead and paid for my airport parking with Aeroplan points, too–why not?

Was this a good deal? I think so. Sure, it’s not as high as the realistic ceiling for Aeroplan points. It is, however, just below the weighted average for Aeroplan points, and in Ultimate Rewards terms, it’s above the weighted average for Chase Ultimate Rewards points. And I had specific dates and times of travel that I needed (since I was going to Calgary for an event) so I had to opt for what was actually available.

More importantly, this fare was cheaperthan alternatives and would otherwise be unattainablewith points. While you can theoretically use Chase points at 1.25 cents per point on their travel portal, that only works for airlines that list their fares with Chase. Obscure low cost carriers like these don’t show up, meaning you’re only shown more expensive options.

9,895 points for a roundtrip flight is virtually unheard of

Less than 5,000 points each way, with no money out of pocket, is an incredibly good outcome for redeeming points on a short-haul flight (especially on a flight like Vancouver to Calgary that is under 500 miles, but over 11 hours of dangerous mountain driving). And remember, I got those points with a 40% bonus. To me, this was an absolute “no brainer” of a redemption.

So how was the flight? Stay tuned for the next installment!

I don’t prefer to stay in chain hotels, and they often don’t exist anyway in the off-the-beaten-path places where I prefer to travel. However, I go to a conference every year in Las Vegas where I run an event. Now, Las Vegas is probably my least favorite destination in the world, and I’d probably never visit otherwise if not for this particular conference. Naturally it happens in the summer, also happens to be during a peak travel week (for some reason), and this makes both flights and hotels really expensive.

Once you have seen the lights of Las Vegas once, you don’t ever need to go back

This year, I somehow managed to get a cheap flight (Southwest ran a good sale after their massive meltdown, so I burned some of my Rapid Rewards points) and the next challenge was finding a reasonably priced hotel. Las Vegas has gotten incredibly expensive as of late. Everything costs extra. You’ll typically pay $30 per day (or more) in resort fees, and on top of this, there’s $15 or so in parking charges. And that’s on top of the rate, which is often $150 or more. A cup of coffee costs $7 (not a fancy barista beverage, just plain coffee). The days of cheap deals in Las Vegas are over.

While I typically use miles and points for flights, there are occasional good values with hotels. The most well-known program is Hyatt, but there was just a brutal devaluation earlier this month, which is a follow-on to the gut punch of a devaluation last year. In Las Vegas, this means you can now book a room at a Hyatt Place for 15,000 points (worth an eye-popping $187.50 worth of Chase points) per night. Plus parking. I’m sorry, Hyatt, but I haven’t stayed at a Hyatt Place anywhere in the world that is even close to worth that.

I checked with a friend who works at a Strip hotel. He offered me his friends and family rate of $249 per night, plus resort fee. Thanks but no thanks. Grasping at straws, I looked at IHG who wanted close to $300 per night worth of points (at current sale prices) for a room at a Holiday Inn Express. And then, bearing in mind my terrible experience at the La Quinta last year (I consider it one of the worst hotels in Las Vegas–check the reviews), I decided to see what Wyndham had to offer.

Transferring Points To Wyndham

Most people don’t know this, but you can transfer both Citi ThankYou and Capital One points to Wyndham. The program offers two different redemption options: “Go Fast” which offers a discounted room rate plus a small number of points (either 1,500, 3,000 or 6,000), and “Go Free” which offers a completely free room paid entirely with points. Most properties cost 15,000 points per night, including such renowned brands as Travelodge and Days Inn. Some top tier (for Wyndham) properties cost 30,000 points. You can also book Vacasa vacation rental properties at 15,000 points per bedroom per night, which can be a pretty good deal in expensive resort destinations. Now, you’re reading Seat 31B, and you can probably guess that $187.50 worth of points (and up) isn’t what I typically spend on a hotel night. There are, however, a handful of properties that cost only 7,500 points per night, and this is where you might occasionally strike gold in the Wyndham program.

In Las Vegas, Wyndham owns a resort called the Desert Rose. It has a two night minimum stay, and is really well rated. Even though the property is actually a resort, they don’t charge for parking or have a resort fee. What’s more, for some reason, this property costs only 7,500 points per night for a “Go Free” stay. But it gets even more interesting than that. Their “Go Fast” rate is actually variable during the week, while paid stays don’t vary much (you’ll pay about $150 per night during the week, and $185 per night on the weekends). “Go Fast” stays from Sunday through Thursday were averaging out at 1,500 points plus less than $70 a night!

Splitting Up Stays

One tactic I’ll sometimes use is paying for some nights, and using points for another. In this case, on a one week stay, the best deal was to use the “Go Fast” rate for Monday through Thursday nights (spending an additional 6,000 points for a completely free room would yield less than $70 in savings, or about 1.1 cents per point). I then booked the “Go Free” rate for Friday through Sunday nights (where I’d have had to spend much more out of pocket, yielding over 2 cents per point in value overall). This meant making two different reservations and technically I will have to check in and out mid-stay. However, hotel front desks are used to dealing with this sort of thing (which can happen for various reasons) and can usually put two reservations together so you don’t have to change rooms.

Wyndham Is Weird

Look, Wyndham Rewards is a pretty strange program, which I suppose suits a hotel chain as strange as Wyndham. They have a pretty big footprint, but their properties are mostly a random hodgepodge of truck stop motels and the occasional timeshare resort. Quality is all over the place, with very little consistency even within brands, and few people would ever consider a Days Inn to be aspirational, which is why I think there is very little written about Wyndham Rewards. Pricing is also all over the place in the program. It’s usually not very good, but occasionally, it’s incredibly good.

I still prefer not to stay in chain hotels, but I like spending money even less (at least when I could spend points at good value). It’s hard to find good independent properties in a place like Las Vegas anyway, and I was happy to get some incredible value for this stay. With no resort fees, no parking fees, and an all-in effective room rate of under $100 per night at a non-casino resort property in a good location, I think this deal has earned the Seat 31B seal of approval.

Air Canada Aeroplan is a popular program to use for award bookings, so it’s not surprising that a lot of people outside of Canada engage with it. You can transfer your points from American Express, Capital One, Marriott Bonvoy and Chase to the Aeroplan program, and use them to book flights on either Air Canada or its truly massive number of airline partners (both StarAlliance and other carriers such as Etihad and Oman Air). So given that, you might be tempted to pick up a Chase Aeroplan co-branded card. These recently launched, and they come with a generous sign-up bonus along with some excellent bonus categories (such as 3x points at grocery stores).

See polar bears with Calm Air, an Aeroplan partner

Well, if you had the Chase Aeroplan card in mind to get you closer to an Aeroplan award, you might want to put those plans on hold. Air Canada has just updated their Aeroplan terms and conditions with some vague and disturbing legalese to their Terms and Conditions that seems targeted at people who qualify for welcome bonuses from Aeroplan banking partners (like Chase):

"Aeroplan may, in its sole discretion, choose to limit the number of Welcome Bonuses or similar bonuses or incentives a Member may receive in any period, and, in addition to the other remedies set forth in these Terms and Conditions, reserves the right to suspend, revoke or terminate the Account of any person who engages in a behaviour of excessive use of the Welcome Bonus offers."

Aeroplan then goes on to vaguely define what it considers abuse in a non-specific way. It’s important to note that this language appeared after multiple Canadian users of Aeroplan reported that their accounts have already been locked “at the request of a bank” after qualifying for signup bonuses, so it appears that Aeroplan is already locking accounts based on some set of criteria.

One of the downsides of frequent flier programs is that they are almost entirely unregulated, and when they operate in countries like Canada (which offers generally poor consumer protections, especially when it comes to airlines) you’re pretty much entirely at the mercy of an airline. They control the vertical and the horizontal. The points in your account hold no value, as they happily remind you in the Terms and Conditions (irrespective of the fact that you can buy them from the airline for actual money), and they also don’t belong to you. It’s very much a one-sided deal.

I don’t know how this is going to ultimately shake out. It’s almost unheard of that an airline program would lock a frequent flier account because of a legitimately earned signup bonus. However, this has clearly happened. Until the dust settles, I recommend that you don’t sign up for the Chase co-branded Aeroplan card. There aren’t enough benefits to holding the card for most people in the US to justify the risk that Aeroplan will randomly decide to torch your account because you earned a signup bonus.

Hi! It has certainly been awhile since I posted last. I’ll be posting more about how my life has evolved since 2019, but suffice it to say that two years of pandemic (which is still grinding on) has led to some major changes. I’m starting to travel again, though, because the world is opening back up again and this is a part of my life that I missed a lot. And more importantly, I’m starting to book more travel (both for myself and for AwardCat clients), which means that I’m working with frequent flier programs a lot more. These have also changed a lot in the past two years, but I have a pretty good idea of which programs I’ll be using and where they are most likely to come in handy.

Incredible award program sweet spots still exist, such as flights from Spain to Morocco using Avios

The conventional wisdom you’ll read on other blogs is to never make speculative transfers from banks into airline programs. Instead, blogs encourage leaving your miles in a bank program (such as Amex, Chase, Capital One or Citi) until you want to redeem an award. This advice is usually on point, and it’s what I will generally advise AwardCat clients to follow. After all, you don’t have to worry about your points expiring in a bank program (as long as you keep at least one card active in the program), and as quickly as airlines are devaluing points in frequent flier programs, banks are adding greater value to their own programs. After all, banks want you engaged with them, not the airlines.

Occasionally, however, an offer will come along that–for me–is worth breaking the usual rules. Two such offers are available, and expiring today: Chase is offering a 25% transfer bonus to Flying Blue, and American Express is offering a 40% transfer bonus to Avios. Last night, I cleaned out my entire Chase account to transfer points to Flying Blue, and I transferred about 100k Amex points with the 40% bonus to Avios. I’ll explain why I did it, and how bucking the conventional wisdom might be a good idea if you have specific future redemptions in mind.

Flying Blue + Westjet

One of the recent changes I made in my life was moving to the greater Vancouver area, which now makes YVR my home airport. Vancouver has the second largest airport on the West Coast with nonstop flights all over the world, but if you’re traveling within North America, the two major Canadian airlines (Air Canada and Westjet) are top dog. They have the most nonstop flights from Vancouver to both US and Canadian destinations.

This presents a really amazing sweet spot for me, because Westjet partners with the Flying Blue frequent flier program, and Westjet also has extremely generous award availability at low redemption rates. For example, you can book economy class travel anywhere in North America for 14,500 points, or 17,500 points each way to the Carribbean. Unlike in the Delta program, the price doesn’t go up the closer you get to departure, either. And there are no fuel surcharges or booking fees; you only pay actual taxes.

Cuba, anyone?

I had 28,000 Chase Ultimate Rewards points, after spending most of my points on the Dubai Hyatt Jumeirah for a forced 10 day quarantine (that’s another story I’ll write about later). Transferring these to Flying Blue got me 35,000 points, which is enough for a nice holiday in the Caribbean this winter. Does this make sense? Of course it does, even though I don’t know exactly what I want to book right now. What’s more, I have pretty much completely drained my Chase account, so I can close the Chase Sapphire Preferred when the annual fee comes due and overall stop engaging with the Chase program (which has lost competitiveness).

Avios + Iberia, Qatar, Sri Lankan and “Royal” Partners

The Avios program has been a mixed bag since 2019. They have gone through multiple rounds of devaluations (including stealth devaluations), often with no prior notice. For example, redemption rates within Asia were previously a sweet spot, but JAL and Cathay Pacific award tickets became more expensive last year. The prices even went up last year for travel on British Airways. In the meantime, although theoretical sweet spots remain on the award chart for award tickets on American and Alaska Airlines, the practical reality is much different. Both airlines have gotten much harder to book using Avios, because fewer seats are being given away to partners (this impacts not only Avios, but also programs such as Cathay Pacific Asia Miles). Wide-open availability between, say, Seattle and Los Angeles or San Francisco and Hawaii is a thing of the past. Keep this in mind when you read mainstream blog articles breathlessly espousing the large signup bonuses for Avios co-branded cards, and touting the award chart as if that equates in any way to actual availability.

Given such a recent history of bad behavior by both the Avios program and partners in the ecosystem, you might be surprised that I’d move a pretty substantial chunk of American Express points into this program. Why? Where one door closes another opens, and Avios has two new partners in the ecosystem: Royal Air Maroc and Qatar Airways. Additionally, I think Iberia, Royal Jordanian and Sri Lankan are underappreciated partners given the very low redemption rates that are often possible with these airlines.

This isn’t an article about the Avios program as a whole. I’ll write one of those going into the sweet spots in detail, so I’ll just talk about some of my personal favorites as a representative example.

Long Haul Premium Cabin Flights On Qatar

The conventional wisdom for redeeming Avios is that they’re good for short to mid haul flights in economy class, on airlines without fuel surcharges. However, they’re super expensive to use for long haul flights in premium cabins, especially on airlines like British Airways with fuel surcharges.

This is now out the window when flying Qatar Airways and using Avios. Qatar recently adopted Avios as its frequent flier currency, and the award chart is much different for flights on Qatar, likely because Qatar is so focused on long haul flights. Additionally, fuel surcharges have been dramatically reduced. Given the new redemption rates, I was able to redeem 85,000 Qatar Qpoints (which transferred in 1:1 from British Airways Avios) plus $224 in cash for Qsuites on an Almaty-Doha-Los Angeles itinerary (yes, I know this is Seat 31B, but this is also almost as far as you can travel in the world. For me, paying about double the points to do it in business class was totally worth it on this route). With the transfer bonus, it cost only 61,000 Amex points which is almost totally unheard of when using Avios for this length of flight. Assuming you can find availability, it’d cost 75k points with American AAdvantage points, or a minimum of 90k points with Asia Miles.

Flights Within Africa On Royal Air Maroc

The conventional wisdom used to be to base yourself for a few months in Hong Kong and then hop around Asia using cheap Avios redemptions on Cathay Pacific, using absurdly low numbers of points for flights that would otherwise be super expensive. This was already on the way out before the pandemic (Cathay Pacific pulled partner availability inside of 14 days), and if Hong Kong and Japan ever open again, flights with Avios are now a lot more expensive.

However, where one door closes, another opens, and that door is in Africa now. Royal Air Maroc flies a ton of places in Africa, and these flights would normally (like many things in Africa) be insanely expensive. Take Casablanca to Lome, Togo. This flight costs 11,000 Avios, plus $29 in tax. It would cost 30,000 AAdvantage points for the same flight, or a whopping $582 in cash! That’s a solid 5 cents per point (or 7 cents per Amex point if you got your Avios with a transfer bonus) in value for an economy class flight–and this is real value, not theoretical value based on a premium cabin seat you’d never otherwise buy.

Is this the only sweet spot with Royal Air Maroc? Nope! There are plenty of others. Casablanca is a low tax airport and Royal Air Maroc doesn’t have fuel surcharges. You can base yourself in Casablanca and hop all over Europe and Africa with extremely generous award availability and very little cash out of pocket for each flight. Now, this isn’t the fanciest airline with the best inflight service, but who cares when it’s this cheap?

Royal Jordanian and Sri Lankan

Royal Jordanian doesn’t get a ton of attention, apart from their high fuel surcharges and apparent willingness to fly through storms that would result in a cancelled flight at other airlines (that being said, their pilots are mostly former Air Force and the airline hasn’t had a major incident in over 35 years). So what makes them interesting? They fly some highly unusual routes. I’m flying them from Tel Aviv to Amman, which is one of the shortest mainline commercial routes in the world. The flight would normally cost about $300 all-in, but I paid 6,000 Avios plus around $100 in taxes and fuel surcharges. It’s not cheap to use Avios on Royal Jordanian, but you can get very good value for your points, particularly if you’re getting the points with a transfer bonus.

Take Amman to Erbil, for example (Erbil is in the Kurdish-controlled part of Iraq, and is relatively safe to visit compared to other parts of Iraq). On a few dates I checked, Royal Jordanian is selling this short flight for $287. Alternatively, you can pay 6,000 Avios plus $135, which is a solid 2.5 cents per point–or 3.5 cents per Amex point if you got your Avios with a 40% transfer bonus.

Sri Lankan is a similar niche airline that is widely ignored due to laughably high fuel surcharges, but with good value Avios redemption pricing to otherwise expensive destinations. You really have to crunch the numbers though because they can have cash fares that are better value than paying with points. Take, for example, one route I have flown, from Colombo to The Seychelles. I picked a random October date and the flight costs 194,113 Sri Lankan rupees (which at today’s exchange rates is $539.61). If you pay with points, it costs 11,000 Avios plus $255. That works out to almost 2.6 cents per point, or 3.6 cents per Amex point if you got your Avios with a 40% transfer bonus.

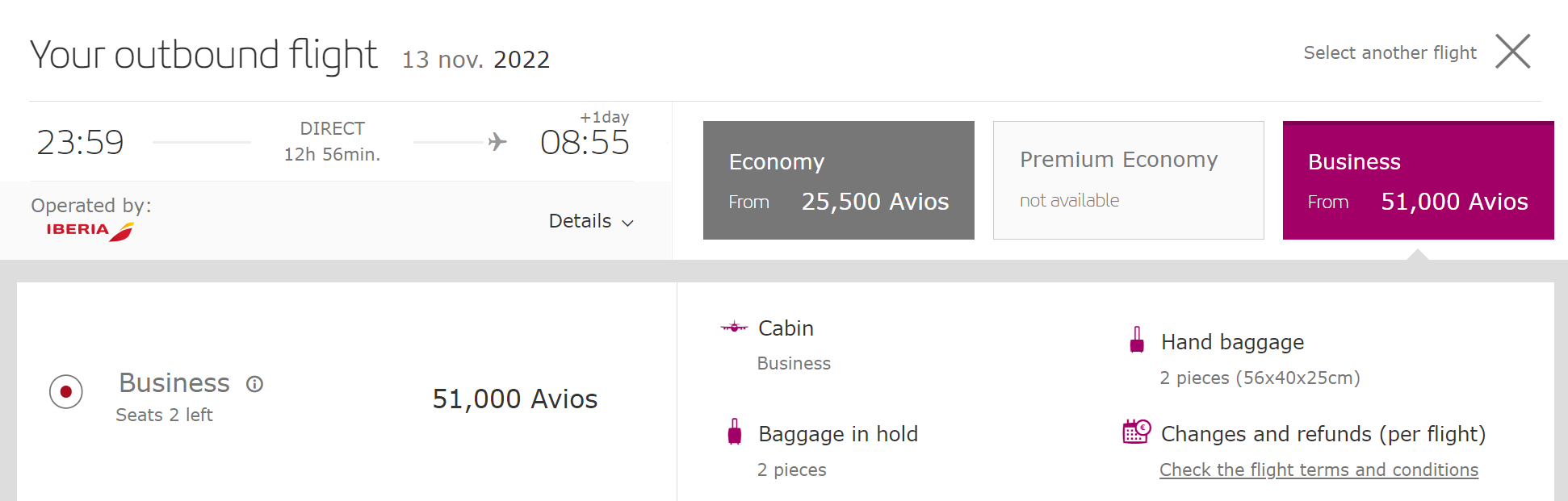

Iberia

Iberia gets a lot of attention for the low redemption rates, with relatively low fuel surcharges, on East Coast to Madrid routes in premium cabins. This requires moving your points into Iberia’s own program and finding availability, which is super hard. Other blogs have documented this extensively (usually while hard selling Avios credit cards) and it’s fine to use Iberia Avios this way, but I’d personally sit in economy class for one of these routes. It’s only 7 hours from New York to Madrid. I’m willing to spend more points to sit up front on a 16 hour flight, but for a 7 hour flight, premium cabins seem like a waste of money to me.

However, how about an 13 hour flight for 51,000 Avios (that’s just 37,000 Amex points with the 40% transfer bonus) in business class, or 25,500 Avios (19,000 Amex points with the 40% transfer bonus) in economy class? That’s what it costs to fly Iberia from Madrid to Montevideo, which is a very nice flight to be on in November when it gets cold in Europe. Ordinarily this would be an over $800 economy class flight. Accounting for taxes and fuel surcharges, you’re getting 2.9 cents per point in value, or 4.2 cents per Amex point in value if you got your Avios with a 40% transfer bonus.

When To Speculatively Transfer

Both of these transfer bonuses expire in a few hours, so if you want to hop on either of them, you should do it right now. However, the most important question is whether you plan to use the points before they will expire, and whether you think the sweet spots you’re after will still be there when you want to take advantage of them. I think that the award flights I’m targeting are in obscure enough partnerships, and in dusty enough corners of award charts, that they’re likely to stick around for awhile. I’m also obsessive to a perhaps unhealthy degree about this stuff (to a point where I help other people book their award travel through AwardCat) so I’m very much on top of my points balances and what is happening in award programs. I feel confident with speculative transfers to both of these programs because I use both of them regularly, and plan to redeem my points before they expire (and hopefully before they devalue).

However, I am going into this with a pretty solid idea of how I’ll use the points. I wouldn’t make a speculative transfer to, say, Asia Miles (since I think Cathay Pacific is likely to declare bankruptcy and may even go out of business entirely), or to Avianca LifeMiles (which has very little credibility as a program given that they block most partner inventory, and don’t even offer much on Avianca). Speculative transfers are, as a general rule, not a great idea–but when done strategically, they can yield incredible value.

I needed to take a last-minute business trip to Kiev. Cash fares were hovering over $900 one way for one-stop itineraries, so I started looking for opportunities to use points. When I book my own award travel, I optimize for the most efficient use of points and the stand-out value was 25,000 Ultimate Rewards points for an Air France flight. There was a long layover in Paris, but I really like Paris so the 9 hour layover was fine. It’s enough time to visit the Louvre and enjoy a coffee in a sidewalk cafe.

Unlike most airlines, Air France touts their economy class cabin. We’ll see if it lives up to the hype!

Unfortunately, the Flying Blue program is an absolute disasterright now. Air France/KLM just switched the chart from a fixed value redemption chart to variable redemptions (which, based on my analysis, is one of the biggest airline devaluations in history–most awards are up a minimum 30% and some are up 500%). It was a total fluke that the flight I wanted still cost 25,000 points, yielding 3.2 cents per point in value all-in (net of taxes/fees I had to pay out of pocket). This is very good redemption value on a ticket for which I would have paid real money. However, the devaluation comes on top of another negative change, removing the award calendar, which has driven call center volumes through the roof (because the only way to search for availability over a range of dates is to call now). Because of this, it can now take 2 hours to get through to an Air France representative.

Of course, my worst nightmare happened. Rather than posting immediately, after I transferred my Chase points, the points didn’t show up. I called Chase, who said that they transferred the points and it was Flying Blue’s fault. I called Flying Blue, and they said they hadn’t received the points so it was Chase’s fault. Both suggested I just wait. So I waited, and waited, and waited. I called to put the seats on hold so they wouldn’t disappear while I was waiting. Eventually I gave up and went to bed.

The following morning, the points still weren’t there. 4 hours before the flight, they still weren’t, so I called Flying Blue again. Fortunately, the friendly representative in the Mexico-based call center had a solution: “We are aware of this issue so we will advance you the points and your account will have a negative balance. When the points post from Chase, your balance will go back to zero.” She put me on hold, then came back a few minutes later to collect my credit card number. And just like that, I had a ticket to Kiev! I didn’t really believe that I did until I went to check in, and the computer spat out boarding passes.

So, certainly a stressful beginning to a trip, but a happy ending. I have no status with Flying Blue. I have never booked a ticket in their program. They don’t know I write this blog. They just thought on their feet and solved the problem by taking a risk (I could have been lying about transferring the points). And so instead of stranding me, which is totally what I expected, I’m now on the way to Kiev.

Summary

Chase is now reading a new telephone script when you call: “It can take from 1-7 days for your points to post after they are transferred.” After slowing down transfers to Korean Air and now Flying Blue, it appears Chase is trying to make Ultimate Rewards less valuable by making it impossible to redeem them for last-minute flights. This doesn’t appear to be a technical glitch; based on the policy change being communicated by their telephone agents, it seems to be deliberate. Also, there is nothing in writing on Chase’s Web sites to communicate the change, so people are going into this process with no idea that points transfers are no longer instantaneous.

Generally speaking, I like the Chase Ultimate Rewards program better than American Express Membership Rewards. However, the ability to have immediate use of transferred points is key. Award travel inventory is dynamic (a seat that is available now likely won’t be in a couple of days, particularly to a popular destination) and most of the value in keeping your points with a bank program instead of an airline program comes from the immediate ability to transfer and redeem points. There are fewer reasons to collect bank points instead of airline points if you aren’t able to easily redeem them for awards.

Airline points programs are rapidly losing credibility so it would be bad for consumers if banks to go the same direction and make points harder to redeem.

I’m very often asked “Which credit card should I get? Should I get the Chase Sapphire Preferred?” This is rarely a surprising question. Bloggers go on and on endlessly about the Chase Sapphire Preferred because it pays them the highest commission. It’s certainly not a bad card, but it isn’t the best one either. And it carries a $95 annual fee. So let’s do a deep dive and see whether it’s a card you should get:

Is this the best card for you? Maybe not.

Untrustworthy Ultimate Rewards Points

The points you’re earning with the Chase Sapphire Preferred are Ultimate Rewards (UR) points. Who backs them? Chase. What are they worth? Whatever Chase says they are, and they can change the value whenever they want. They are not airline, hotel or rental car points. This can be dangerous; if the bank shuts your account down (and they can do this for essentially any reason or no reason), they can take all of your points and there’s nothing you can do about it. The bank can devalue the points and benefits whenever they want, as other travel programs do. Points are considered a discount, not cash. This actually benefits you for tax purposes, but it’s not a good thing at all when it comes to your rights around devaluation. In short, you don’t have any. There have been multiple cases with different banks shutting down accounts of people who are too good at working the programs.

You can legally count cards in Las Vegas and gain an advantage in blackjack, but the casinos can legally refuse to play with you. Banks play basically the same game with points. My recommendation is never to maintain high balances of bank points, because they could pull the rug out from under you at any time.

Sketchy Sign-Up Bonus

Right now, you can get 50,000 bonus points for signing up and an additional 5,000 points for adding an authorized user to the card. The catch? You have to spend a whopping $4,000 in the first 3 months of having the card. This used to be easy when you could buy Visa gift cards or Vanilla Reload cards and load them to an American Express Bluebird, which you could then use to pay your credit card bill. However, American Express shut this down last month, and ever since it’s gotten a lot harder. Are you sure you can spend $1,333+ per month on a credit card without buying a bunch of crap you don’t need?

The worst part: If you don’t achieve the spending threshold, you don’t get the bonus. Simple as that. Chase is banking on this.

Pathetic Points Transfers

Chase boasts that you can transfer points at a 1:1 ratio to travel partners. The problem is, most of their partners just aren’t very good. 40% of the transfer partners are hotel programs, and they’re the ones with the least valuable points in the industry. The airline partners aren’t much better (although there can be sweet spots with each one). Redeeming British Airways Avios points often involves paying hefty fuel surcharges and the best awards–on Alaska Airlines–can only be booked over the phone. Korean Air SKYPASS not only has a horrendously expensive award chart, but booking awards is a giant hassle and you can only book tickets for yourself and immediate family members (with extensive documentation requirements), not friends. And after the United award chart devaluation, it’s really only worthwhile to use Mileage Plus points on United–the least reliable airline in America.

It’s not that there aren’t sweet spots in each of these programs that can make them worthwhile. It’s just that airline points devalue faster than Zimbabwe dollars, and hotel points are nearly as bad. And if you want to earn airline points, the benefits tend to be much better with airline affiliate cards (for example, you get companion passes, drink coupons and free checked bags with many airline cards).

Dodgy Discounts

“Get 20% off travel!” claims the headline. Unfortunately, there’s an asterisk, and it’s a big one: you can’t book your travel directly with hotels or airlines. Instead, you have to book through a Chase travel agency portal. And as you may have guessed, this doesn’t give you all of the options, and the prices shown are often higher than you can get booking through other sites. The “20% savings” might actually end up costing you money.

Wrap-up

Should you get the Chase Sapphire Preferred? Sure, if you want to support your favorite travel blogger with a fat commission by using their affiliate link. Otherwise, it’s not the best travel card out there, and it isn’t by a long shot.

I like getting bonus miles to share a good deal with friends, and I don’t like fine print. Chase is offering some of both in their most recent refer-a-friend promo for the Rapid Rewards Visa that you may have signed up for when I offered it in November. Beware: you might not get the miles you expect for signing up your friends if Chase also offers you a referral bonus.

I received an offer in the mail last week offering me 5,000 miles for every person that I refer through June 30th. However, there is a lot of disturbing fine print so I called Chase today to confirm the details of the offer. What I found out was really disturbing and Chase may not honor the referral deal as clearly published. So, if you choose to participate in this program, it’s best to be fully aware of how it might bite you.

Changing Promotions

Chase can change the terms of the promotion at any time. So, although I received a refer-a-friend offer in the mail for up to 10 friends–and they even included 10 tear-off referral cards to share–my promotion was silently cut back! What did Chase do? They pared back the promotion to only allowing 6 referrals instead of 10, and this was done with no prior notification. I would never have known unless I called Chase and they told me that they did this. I would have done the work of selling 4 friends and readers on their card (which, to be clear, is actually a good deal) for no compensation whatsoever.

Calendar Year Can Clobber Your Points

Making matters worse, Chase only awards 50,000 referral points per calendar year. I completed 10 referrals in November and December. However, the points haven’t been credited to my account yet, and won’t be credited until sometime in 2016. Chase measures “calendar year” based on when they credit the points to your account, not based on when the referral was completed. So, if I participate in any referral programs in 2016 at all, I’ll be helping Chase sell credit cards, but I won’t actually get the referral bonus for doing so. If I hadn’t asked, I would have done a lot of work for nothing.

Calling Out Chase

Most travel bloggers won’t ever call out a bank for doing something wrong or questionable. After all, Chase pays good money for referrals, which is why most travel blogs are always going on and on about the Sapphire Preferred card (which, to be honest, just isn’t all that good). I’m not afraid to call out Chase, though–they’ve never paid me a dime. The refer-a-friend program is rife with exclusions and “gotcha” clauses and there’s simply no excuse for it. If Chase takes the referral, they should cough up the miles without any weaseling. After all, referring friends and readers doesn’t stop with them signing up for the card. It’s a lot of work! People come to me about any problems they have with the card, or any questions they have about the Rapid Rewards program in general.

What’s Next?

I still think that the Rapid Rewards Visa offer with 50,000 bonus points is a good deal (vs. their normal 25,000 bonus point offer, which isn’t good). However, the refer-a-friend program just isn’t credible. It’s just too rife with conditions, exclusions, and last-minute changes. If you’re going to participate, I recommend you call Chase every time to confirm the details before you make a referral. And given the amount of time this requires, you might prefer to avoid the program altogether.